What is the space left for the iron-lithium battery company?

1. The sales volume of new energy buses declined significantly.

In January-February 2017, the production and sales volume of new energy vehicles in China was significantly lower than the same period of the previous year. According to the China Association of Automobile Manufacturers, the production and sales volume of new energy vehicles in the first two months of 2017 were 25,213 and 24,781, respectively, down 33.5% and 30.5% year-on-year. Among them, the bus market is even more bleak. According to the output data of the Ministry of Industry and Information Technology, in January-February 2017, the total sales volume of new energy buses was only 475 (the statistics are more than 5 meters, excluding the number of unreported enterprises). Compared with the 3,176 and 4430 vehicles in 2015 and 2016, it is a cliff-like decline. The falling terminal market will directly affect the production planning and scheduling of power battery companies, and may even cause the stagnation of power battery manufacturers. This will be more prominent in the iron-lithium battery industry.

2, iron and lithium is still the main force of new energy buses, but facing the challenge of three yuan

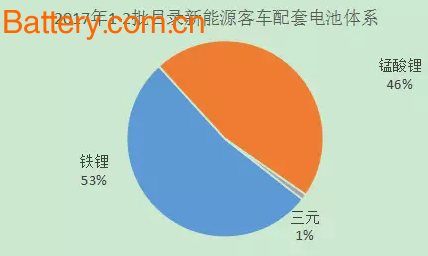

After experiencing the ban on the ban on passenger cars at the end of 2016, ternary power lithium battery companies began to enter the supply system of new energy buses, squeezing the living space of iron-lithium battery companies. In the catalogue of new energy buses announced in January-February 2017, lithium iron phosphate batteries accounted for 53%, lithium manganate batteries accounted for 46%, and ternary batteries accounted for 1%. (Lithium manganate is mainly a hybrid vehicle with a lower proportion of electricity.) Among them, in the second batch of catalogues, there are three models of pure electric buses supplied by ternary batteries. With the publication of the later catalogue, the number of ternary pure electric buses will increase.

3. In the future, iron and lithium will be difficult in the field of new energy passenger cars and special vehicles!

Passenger car

Lithium batteries from three yuan 2016 has become the mainstream passenger cell, a scaled three yuan passenger cars continue to enhance cell in batches 1-2 directory 2017, 77%; proportion of iron phosphate lithium battery fell to 20%, and in the second batch of passenger cars in 2017, only the model of BYD used lithium iron phosphate. It should be noted that BYD's 2017 models, Qin 100 and Tang 100, have also begun to use ternary lithium batteries. It is foreseeable that the future new energy passenger vehicle market will be able to find the role of iron and lithium.

VIP Car

Like the passenger car, the ternary battery has also become the mainstream battery for the special car. In 2017, the proportion of the ternary battery in the 1-2 batch catalogue increased to 70%, the lithium iron phosphate battery accounted for 22%, and the lithium manganate battery accounted for The ratio is larger than 8%. The main dedicated models of iron-lithium are also based on the BYD model catalogue.

4. There is not much room left for the iron-lithium battery enterprise!

Under the influence of the subsidized New Deal, the demand for energy density of new energy bus companies has increased. The highest subsidy for passenger cars is 1.2 times, and the system energy density is required to reach 115Wh/kg. The future bus companies will focus on the power battery companies that meet the highest subsidy requirements. In 2017, the first and second batches of catalogues announced the energy density of the vehicle system. In particular, the energy density of the second batch of catalogues on passenger cars increased significantly, and nearly half of them reached the highest-grade subsidy standard of 115Wh/kg.

Two batches of supporting battery business directory of new energy bus in front, CATL lithium iron phosphate battery system to achieve the highest energy density 137.27Wh / kg, and even more than a lot of the energy density of the battery system of three yuan. According to the published catalogue, only the battery companies with the highest energy subsidy standards, such as CATL, Beijing Guoneng Battery, Tianjin Lishen, Weihong Power and Jiangsu Jinyangguang, have not reached the highest standards.

In the list of the first two batches of new energy buses, 48% of the models were provided by the CATL one, and the second is the Menguli, which accounted for 28% of the total models, mainly for plug-in power vehicles. BYD only gave Self-supporting, the model is relatively low. In terms of power battery supply alone, the bus brands with the highest sales volume in the market, except for BYD, have adopted the power battery of CATL. The situation in the market has been presented, leaving room for other iron-lithium battery companies. too much!

After the baptism in 2017, the market pattern of iron-lithium battery will tend to be stable.

School Bus,Mini School Bus,Electric School Bus,Motor Bus School Bus

CLW GROUP TRUCK , http://www.clwgrouptruck.net